Supply Tightens, Phoenix Strengthens, and the Path Forward Comes into Focus

The national housing market is navigating a distinct inflection point. Supply is contracting. New starts are slowing. The macroeconomic picture is mixed but stabilizing. And for developers with conviction in high-growth Sun Belt markets, the conditions ahead may look better than the headlines suggest.

Supply Is Tightening, and That Has Consequences

Development pipelines that filled during 2022–2023 are being delivered into the market now, but what comes next is a much thinner supply picture. Legislative uncertainty around the ROAD to Housing Act froze equity capital for much of early 2026, stalling an estimated 10,000 BTR units nationally. Meanwhile, broader investor caution has slowed new project commitments across the board.

For operators, a constrained supply pipeline has an upside: renters stay longer when there are fewer alternatives. Retention improves. Lease-up timelines stabilize. The tradeoff is that higher-for-longer rates continue to weigh on asset values and transaction activity, keeping many deals on hold until financing math improves.

The Fed: A New Chapter with Uncertain Timing

New Federal Reserve Chair Kevin Warsh has signaled a structural overhaul of how the Fed communicates and operates, less forward guidance, more data dependence. That shift toward ambiguity makes rate forecasting harder for developers and lenders alike.

The jobs picture, while improving, complicates the rate outlook. U.S. employers added 172,000 jobs in May, double market expectations, pushing the three-month average to its highest level in over two years. Strong employment typically keeps the Fed from cutting, and with inflation still elevated in part due to energy costs, markets are now pricing in a rate increase before year-end, with a potential second by mid-2027.

For the BTR sector, the rate environment cuts both ways. Higher borrowing costs continue to suppress homeownership affordability, keeping renters in place longer and supporting occupancy across well-located communities. That’s a genuine operational tailwind. At the same time, elevated rates compress valuations and keep transaction activity constrained, a reality that requires patience from owners and disciplined underwriting from developers. The deals being structured today at current capital costs are the ones that will perform when the rate environment eventually shifts. Until then, the focus remains on fundamentals: location, product quality, and markets where demand is structural rather than cyclical.

Consumer Resilience Is Showing Up in the Data

Despite headline uncertainty, consumer behavior has held up. Retail sales climbed sharply in May, outpacing economist expectations and accelerating from April’s gains. Inflation expectations among businesses have been gradually retreating. These are meaningful signals: the consumer driving rental demand is still employed, still spending, and increasingly, still renting.

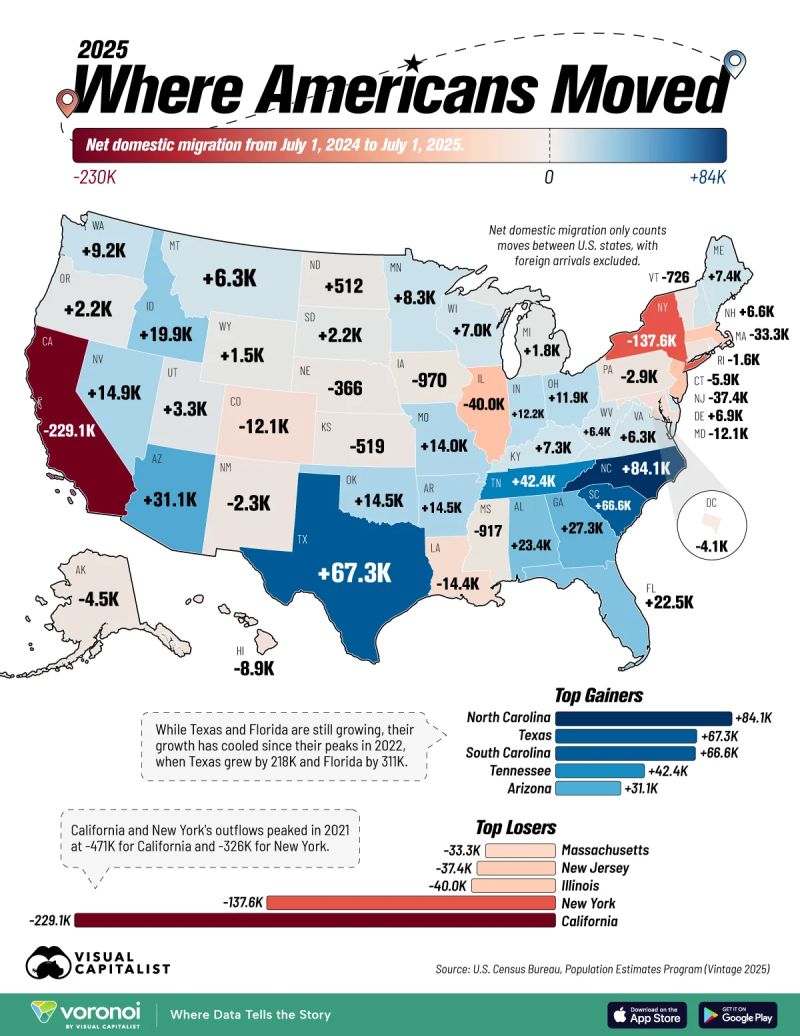

Migration patterns reinforce the point. U.S. Census data for 2025 shows Arizona added 31,100 net domestic migrants, among the top five in the country. That population inflow translates directly into housing demand, labor market depth, and retail activity. It is not an accident that capital continues to find its way to Metro Phoenix.

Arizona: The Local Story Remains Strong

Seven Arizona cities were named among America’s Top 50 New Boomtowns. Phoenix, Tucson, and Flagstaff all appeared on Resonance’s best cities list. Scottsdale ranked sixth in the country for career-starting destinations in 2026. These are not vanity metrics; they are leading indicators of where workforce population is building and where rental demand follows.

The structural drivers behind Arizona’s growth are durable. TSMC and Amcor recently finalized a 10-year partnership deal, deepening the semiconductor and advanced manufacturing ecosystem in Metro Phoenix. The TSMC effect alone is putting Phoenix industrial in what analysts are calling the early innings of a decade-long expansion, with ripple effects across housing, retail, and infrastructure demand. Arizona’s data center boom is layering additional long-term employment anchors into the market.

This is exactly the environment that should shape where developers commit capital. While AI-driven displacement does raise legitimate questions about employment stability in white-collar and tech-heavy markets, markets like Phoenix, where job growth is tied to advanced manufacturing, healthcare, and infrastructure, offer a more defensible demand story. Knowing where jobs will be is the foundational question in housing development. Metro Phoenix continues to answer it clearly.

The Bottom Line

Supply is falling. Demand drivers in Arizona remain intact. The macroeconomic environment, while uncertain, is stabilizing in ways that favor patient, well-positioned developers in high-growth markets. The pipeline thinning nationally isn’t a headwind for Phoenix, it’s a setup.